Commercial truck insurance coverage is a must-have for any business that operates trucks on public roads. It protects your company, drivers, and vehicles from accidents, damages, and lawsuits. But understanding all the options, rules, and risks can be tricky—even for experienced business owners.

This article will help you navigate the basics, compare coverage types, and avoid common mistakes. You’ll learn how to choose the right policy, what affects your rates, and why careful planning matters for your bottom line.

What Is Commercial Truck Insurance?

Commercial truck insurance is a special type of business auto insurance designed for trucks used for work. Unlike personal auto insurance, it covers bigger risks and higher values. Trucks often carry expensive goods or work in dangerous environments, so policies must protect against theft, damage, injury, and lawsuits.

There are many kinds of commercial trucks: dump trucks, tractor-trailers, box trucks, tow trucks, and more. Each needs specific coverage, depending on its job and size. For example, a food delivery van faces different risks than a heavy hauler crossing state lines.

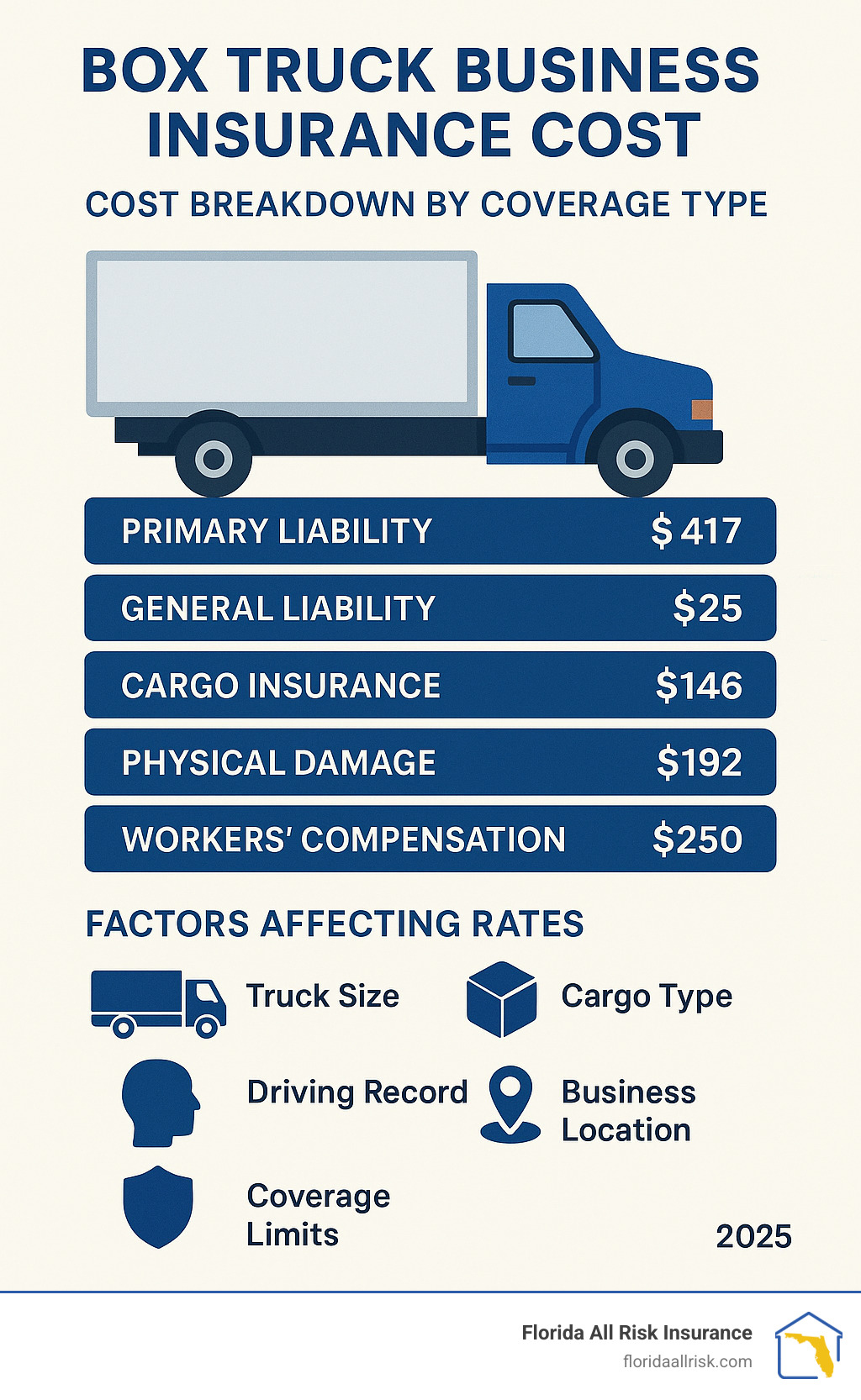

Key Types Of Commercial Truck Insurance Coverage

Choosing the right coverage means matching your policy to the risks your trucks face. Here are the main types of coverage:

Liability Coverage

Liability insurance is required by law for most commercial vehicles. It pays for injuries or property damage if your truck causes an accident. Two main parts:

- Bodily Injury Liability: Pays for medical costs, lost wages, and legal fees if someone is hurt.

- Property Damage Liability: Covers repairs or replacement if another person’s property is damaged.

Federal law requires trucks that cross state lines to carry minimum liability limits—often $750,000 or more for large vehicles.

Physical Damage Coverage

This covers your own truck if it’s damaged, no matter who’s at fault.

- Collision Coverage: Pays for repairs after a crash.

- Comprehensive Coverage: Covers theft, fire, vandalism, or weather damage.

If you lease or finance your truck, lenders usually require physical damage coverage.

Cargo Insurance

Motor truck cargo insurance protects the goods you’re hauling. If cargo is damaged, lost, or stolen, this pays for replacement or repairs. Some policies also cover cleanup costs if cargo spills.

Special rules apply for certain cargo, like hazardous materials or food. Make sure your policy matches what you transport.

Uninsured/underinsured Motorist Coverage

If another driver causes an accident but doesn’t have enough insurance, this coverage protects you and your drivers. It can pay for medical bills, lost income, and repairs.

Non-trucking Liability

Also called bobtail insurance, this covers your truck when it’s not hauling cargo for business. For example, if your driver is using the truck for personal reasons and gets in an accident.

General Liability

This is broader than auto liability. It covers accidents at your office, loading dock, or during business activities that don’t involve driving.

Additional Coverage Options

- Trailer Interchange: Covers damage to trailers your drivers don’t own.

- Medical Payments: Pays for injuries to your driver or passengers.

- Rental Reimbursement: Pays for a rental truck if yours is out of service.

- Downtime Coverage: Helps cover lost income while your truck is being repaired.

Comparison Of Coverage Types

To help you see the differences, here’s a quick comparison:

| Coverage Type | Main Purpose | Required? |

|---|---|---|

| Liability | Injury or damage to others | Yes (by law) |

| Physical Damage | Damage to your truck | No (but often needed) |

| Cargo Insurance | Damage/loss to goods | No (required by some contracts) |

| Non-Trucking Liability | Personal use accidents | No |

| General Liability | Business risks off-road | No |

Who Needs Commercial Truck Insurance?

Most businesses that use trucks need special coverage:

- Owner-operators: Drivers who own their trucks and contract with carriers.

- Fleet owners: Companies with two or more trucks.

- Small businesses: Even a single delivery van counts.

- Contract carriers: Those who haul goods for others.

Some beginners think that personal auto insurance is enough, but it doesn’t cover business use, cargo, or high-value risks. If you operate trucks for work—even part-time—you need commercial coverage.

What Affects Your Insurance Costs?

The price of commercial truck insurance can vary greatly. According to the National Association of Insurance Commissioners (NAIC), average annual premiums range from $6,000 to $12,000 per truck. But many factors change the price:

| Factor | Effect on Cost |

|---|---|

| Truck type | Larger/heavier trucks cost more |

| Cargo type | Hazardous or valuable goods raise rates |

| Driving history | Accidents or violations increase premiums |

| Location | Urban areas or long routes may cost more |

| Deductibles | Higher deductibles lower premiums |

| Coverage limits | Higher limits raise costs |

Many beginners miss the impact of claims history. Insurers look at your past claims, not just accidents. A single cargo theft or lawsuit can spike your rates. Also, safety technology (like dash cams or automatic braking) can earn discounts.

How To Choose The Right Coverage

Deciding what coverage to buy can feel overwhelming. Here’s how to make confident choices:

- List your risks: Write down every danger your trucks face—accidents, theft, cargo spills, weather, lawsuits.

- Know legal requirements: Each state and federal agency has rules. For interstate trucks, the Federal Motor Carrier Safety Administration (FMCSA) sets minimums.

- Match coverage to your business: A food delivery truck doesn’t need hazmat coverage, but a fuel hauler does.

- Ask about discounts: Insurers offer discounts for good driving, safety devices, bundled policies, and paying annually.

- Review contracts: Shippers often require specific coverage—like cargo minimums or special endorsements.

- Compare quotes: Prices vary, so get several offers. Make sure each quote includes the same coverage types and limits.

A common mistake is buying only the minimum required coverage. It may keep you legal, but leaves you exposed to big losses. For example, if your truck damages a building and your limit is too low, your business pays the difference.

Credit: www.truckinsurancenitic.com

Common Mistakes To Avoid

Many new truck owners or operators make these errors:

- Underinsuring cargo: Not matching coverage to the value of goods hauled.

- Ignoring exclusions: Some policies don’t cover certain risks (like employee theft or specific cargo types).

- Forgetting about downtime: Not covering lost income when trucks are in repair.

- Skipping non-trucking liability: Not protecting trucks during personal use.

- Missing contract requirements: Not meeting coverage levels required by clients or shippers.

Experienced advisors suggest reviewing your policy every year, especially if your business changes. Add new trucks, hire drivers, or switch cargo? Update your insurance.

Real-world Example

Imagine a small moving company with three box trucks. One truck crashes into a parked car. The company’s liability insurance pays for the car repairs and medical bills. But the truck is also damaged, and the cargo inside is ruined.

If the company only bought liability coverage, they must pay for the truck and cargo losses themselves.

Now, if they had physical damage and cargo insurance, these costs would be covered. This shows why a basic policy isn’t enough for most businesses.

Insurance Requirements By State And Federal Law

Each state has its own rules. Most require liability coverage, but amounts differ. Interstate trucking must follow federal rules—usually $750,000 minimum for standard cargo, and $5 million for hazardous materials.

Some states require extra coverage, like uninsured motorist or environmental cleanup for spills. Always check with your state’s Department of Transportation or FMCSA.

How To Lower Your Premiums

Insurance costs can be a major business expense. Try these tips to save money:

- Install safety devices: Dash cams, GPS tracking, and anti-theft systems can earn discounts.

- Train drivers: Safe driving courses reduce accidents and claims.

- Increase deductibles: Higher deductibles mean lower premiums, but you pay more out of pocket for claims.

- Bundle policies: Buy multiple types of insurance from the same company.

- Pay annually: Some insurers give discounts for yearly payments instead of monthly.

Here’s a quick look at how safety features affect premiums:

| Safety Feature | Average Premium Reduction |

|---|---|

| Dash cam | 5–10% |

| GPS tracking | 3–7% |

| Automatic braking | 6–12% |

| Driver safety training | 5–15% |

Credit: alchemyinsurance.com

Non-obvious Insights For Beginners

- Contract language can change your coverage: Many shippers or brokers require “additional insured” status, special endorsements, or higher cargo limits. Always read contract details before accepting a job.

- Claims can affect business reputation: Insurance claims aren’t just about money. Multiple claims may lead to higher rates, but also fewer contracts. Shippers often check your safety and claims history before hiring you.

Finding The Right Insurance Provider

Look for companies with experience in truck insurance. Good providers offer fast claims service, flexible coverage, and help with compliance paperwork. Ask other business owners for recommendations.

The FMCSA keeps lists of licensed carriers and insurance providers. For deeper research, check National Association of Insurance Commissioners.

Credit: floridaallrisk.com

Closing Thoughts

Commercial truck insurance coverage is more than just a legal requirement—it’s a vital part of protecting your business, your assets, and your future. Choosing the right policy means understanding your risks, meeting legal rules, and planning for the unexpected. Avoid common mistakes, review your coverage often, and take advantage of discounts for safety and training.

With careful planning, you can keep your trucks rolling and your business growing—no matter what the road brings.

Frequently Asked Questions

What Is The Minimum Required Commercial Truck Insurance?

Most states require at least liability insurance. For interstate trucking, federal law sets a minimum of $750,000 for standard cargo and up to $5 million for hazardous materials.

Does Personal Auto Insurance Cover Business Truck Use?

No. Personal auto policies do not cover trucks used for business, cargo, or high-value risks. You must buy commercial truck insurance.

How Can I Lower My Commercial Truck Insurance Premiums?

Install safety devices, train drivers, bundle policies, pay annually, and raise deductibles. Compare quotes from several insurers to find the best price.

What Happens If My Cargo Is Damaged During Transport?

If you have cargo insurance, your policy pays for repair or replacement. Make sure your coverage matches the type and value of goods you haul.

Can I Get Commercial Truck Insurance If I Have A Poor Driving Record?

Yes, but expect higher premiums. Some insurers may refuse coverage. Improving your driving record and taking safety courses can help lower rates over time.

Read More:

- Workers Compensation Insurance Costs: What You Need to Know

- Motorcycle Insurance for Young Riders: Essential Tips and Savings

- Pet Insurance Plans With Low Deductibles: Save More on Vet Bills

- Flood Insurance Coverage Requirements: What Homeowners Must Know

- Umbrella Insurance Policy Benefits: Protect Your Assets Today

- Best Renters Insurance Policies 2026: Top Picks for Maximum Protection

- Dental Insurance for Self-Employed: Maximize Your Coverage Today

- Medicare Supplement Insurance Plans: Your Guide to Smarter Coverage