Floods are one of the most common and costly natural disasters in the United States. Every year, they cause billions of dollars in damage to homes, businesses, and infrastructure. Many people are surprised to learn that standard homeowners insurance does not cover flood damage. This gap can leave families financially devastated after a major flood. Understanding flood insurance coverage requirements is essential for property owners, especially those in high-risk areas. Whether you are buying a new home, refinancing, or simply want to protect your investment, knowing when and why you need flood insurance can save you from serious losses.

What Is Flood Insurance?

Flood insurance is a special type of property insurance. It covers losses caused by flooding, which is not included in most basic homeowners or renters policies. Flood insurance is often provided through the National Flood Insurance Program (NFIP), a federal initiative managed by the Federal Emergency Management Agency (FEMA). Some private insurers also offer flood policies, but the NFIP is the main source for most Americans.

Flood insurance policies typically cover:

- Building property (the structure and foundation)

- Personal property (your belongings inside the home)

It’s important to know that coverage limits apply, and certain items like cash or precious metals are usually not covered.

Why Flood Insurance Is Required

Flood insurance is not always optional. In some cases, you are legally required to purchase it. The main reason for this requirement is risk management. Lenders and the federal government want to reduce the chance of unpaid loans and financial disasters.

High-risk Flood Zones

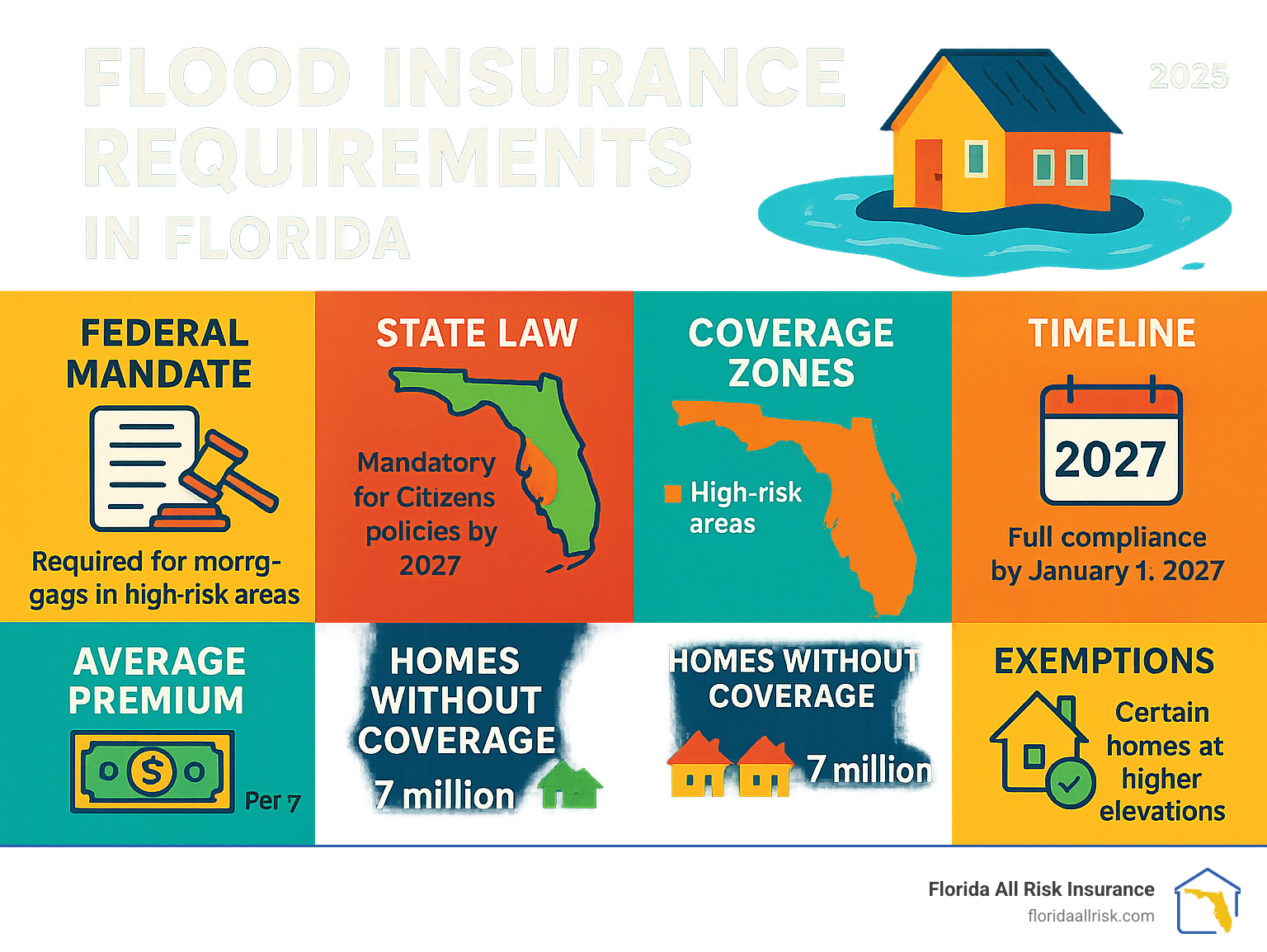

If your property is in a Special Flood Hazard Area (SFHA), your lender will almost always require you to buy flood insurance. These zones are identified on FEMA’s flood maps as areas with a 1% or greater chance of flooding each year. This is also known as the 100-year floodplain.

Federally Backed Loans

If you have a mortgage from a federally regulated or insured lender (such as FHA, VA, or USDA loans), and your home is in a high-risk flood zone, federal law requires flood insurance. This rule applies to both new purchases and refinancing.

Local Laws And Community Requirements

Some states and local governments have their own flood insurance rules. For example, they may require flood insurance for all properties in certain neighborhoods, even if you do not have a mortgage. Always check with your local authorities for specific rules.

How Flood Insurance Coverage Works

Flood insurance does not function like regular homeowners or renters insurance. Understanding what is covered and what is excluded helps avoid surprises after a disaster.

What Is Covered

Most flood insurance policies include two main parts:

- Building property coverage: Covers the structure, foundation, electrical and plumbing systems, central air and heating, water heaters, and built-in appliances.

- Personal property coverage: Includes furniture, clothing, electronics, curtains, washers and dryers, and some portable appliances.

The following table shows a typical breakdown of flood insurance coverage through the NFIP:

| Coverage Type | NFIP Maximum Limit | Covered Items |

|---|---|---|

| Building Property | $250,000 | Walls, floors, foundation, HVAC, built-in appliances |

| Personal Property | $100,000 | Furniture, electronics, clothing, curtains, small appliances |

What Is Not Covered

Flood insurance has important limits. It does not cover:

- Basement improvements (like finished walls, carpets)

- Temporary housing or hotel bills if you must move out

- Vehicles

- Mold or mildew damage not caused by the flood

Also, claims for damage caused by moisture, mildew, or mold are only paid if they are directly caused by a covered flood.

Who Needs Flood Insurance?

Many people think they are safe if they do not live in a high-risk zone. In reality, more than 20% of flood claims come from moderate- or low-risk areas.

You need flood insurance if:

- Your lender requires it due to your property’s flood zone status

- You live in a flood-prone area

- You want to protect your property investment

Even renters can buy flood insurance to protect their belongings. Business owners should also consider commercial flood insurance.

Credit: floodsciencecenter.org

How To Determine Flood Zone And Insurance Requirements

Knowing your property’s flood risk is the first step. FEMA creates Flood Insurance Rate Maps (FIRMs) to show flood zones. You can find your flood zone by:

- Visiting the FEMA Flood Map Service Center online

- Asking your local building or planning office

- Checking with your mortgage lender or insurance agent

Flood zones are labeled as follows:

- Zone A: High risk, flood insurance required

- Zone V: High risk, coastal areas, insurance required

- Zone X (shaded): Moderate risk, insurance recommended but not required

- Zone X (unshaded): Minimal risk

The following table compares key flood zone designations:

| Zone | Flood Risk Level | Insurance Requirement |

|---|---|---|

| A / V | High | Mandatory (if loan is federally backed) |

| X (shaded) | Moderate | Optional but recommended |

| X (unshaded) | Low | Optional |

How Much Flood Insurance Do You Need?

The required coverage amount depends on your lender, property value, and the NFIP limits.

- For homes, lenders usually require coverage equal to the lesser of: The outstanding mortgage principal, the replacement cost of the building, or the NFIP maximum ($250,000).

- For personal belongings, you can choose the coverage amount, up to $100,000 for residential properties.

- Commercial properties can buy up to $500,000 for building and $500,000 for contents.

Replacement Cost Vs. Actual Cash Value

Building coverage through the NFIP is based on replacement cost value (RCV) if the home is your primary residence and insured for at least 80% of its RCV or the maximum available. Otherwise, it pays actual cash value (ACV), which subtracts depreciation.

Personal property is always paid out at ACV.

Credit: floridaallrisk.com

How To Buy Flood Insurance

Flood insurance is sold through both the NFIP and private insurance companies. You can buy it by:

- Contacting your current home insurance agent

- Reaching out to an insurance company that participates in the NFIP

- Exploring private flood insurance options for higher limits or broader coverage

There is typically a 30-day waiting period before coverage begins. Exceptions exist for some loan closings.

The following table compares NFIP and private flood insurance features:

| Feature | NFIP | Private Market |

|---|---|---|

| Maximum Building Coverage | $250,000 | Varies, often higher |

| Contents Coverage | $100,000 | Varies, can be higher |

| Waiting Period | 30 days | Can be shorter |

| Availability | Nationwide | May be limited by state or risk |

| Additional Features | Standardized coverage | Expanded coverage options |

Common Mistakes And Non-obvious Insights

Many homeowners make errors that lead to uncovered losses or insurance gaps. Here are some insights:

- Assuming you’re not at risk: Floods can happen anywhere, not just in high-risk zones. Localized storms, poor drainage, or construction can change your risk overnight.

- Relying on disaster aid: Federal disaster assistance is not guaranteed and, when available, is often a loan you must repay.

- Not updating coverage: Property improvements (like additions) can increase your rebuilding cost. Review your policy regularly.

- Not understanding exclusions: Items stored in basements, garages, or outside may not be covered.

- Waiting too long to buy: The waiting period means you can’t buy insurance right before a storm and expect to be covered.

Credit: agents.floodsmart.gov

The Cost Of Flood Insurance

Flood insurance premiums depend on:

- Flood zone

- Building characteristics (age, elevation, construction type)

- Coverage amount and deductible

- Policy type (NFIP or private)

In 2023, the average annual NFIP premium was around $950, but this varies widely. Homes in high-risk areas may pay several thousand dollars per year. New NFIP pricing, called Risk Rating 2.0, aims to make prices reflect true flood risk more accurately.

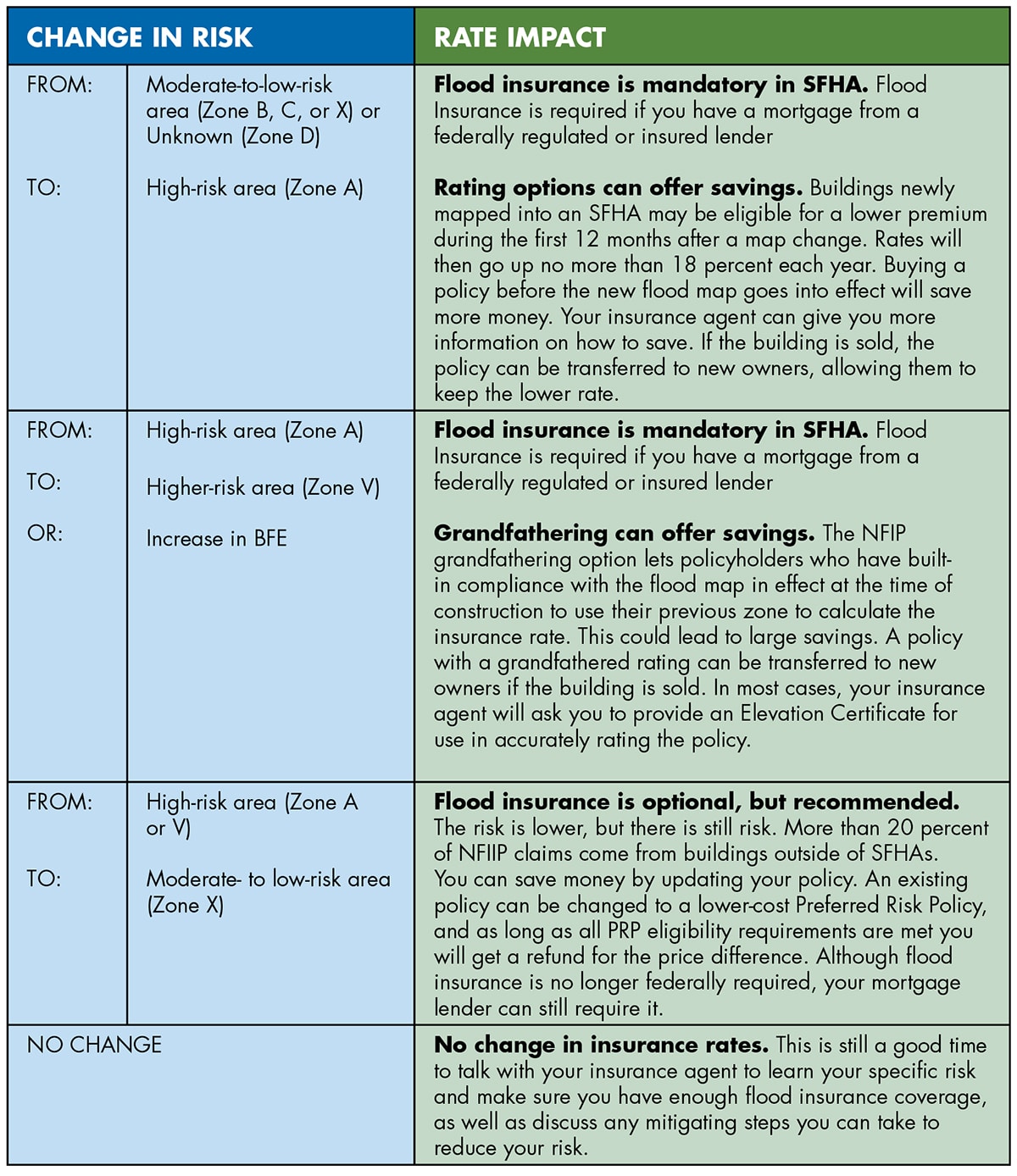

What To Do If Your Property Is Mapped Into A High-risk Zone

Flood maps change over time. If new maps put your home in a high-risk area, your lender will usually notify you that insurance is now required. You have options:

- Grandfathering: You may qualify for lower rates if you purchase insurance before new maps take effect.

- Appeal: If you believe the map is wrong, you can appeal to FEMA. A survey or elevation certificate may be needed.

- Shop around: Compare NFIP and private insurance to find the best price and coverage.

Benefits Of Flood Insurance Even When Not Required

Flood insurance can prevent financial ruin. Even one inch of water can cause more than $25,000 in damage to an average home. Flood insurance provides peace of mind, helps with recovery, and may increase your home’s value to buyers who see it as a safer investment.

Where To Learn More

For up-to-date flood maps, official requirements, and answers to specific questions, visit the FEMA Flood Insurance page.

Frequently Asked Questions

Is Flood Insurance Required For All Homes?

No, flood insurance is only required for homes in high-risk zones with federally backed mortgages. However, any property can buy coverage, and it is often wise even in lower-risk areas.

Can I Buy Flood Insurance If I Rent My Home?

Yes, renters can purchase flood insurance to protect their belongings. The building owner is responsible for insuring the structure, but your personal items are not covered by their policy.

How Soon Does Flood Insurance Become Effective?

There is usually a 30-day waiting period before a new flood insurance policy takes effect. Some exceptions apply, such as when buying a new home with a loan.

Does Flood Insurance Cover Basement Damage?

Flood insurance covers some items in basements (like washers, dryers, and water heaters) but not finished walls, floors, or living areas. Check your policy for details.

Can I Buy More Coverage Than The Nfip Maximum?

Not through the NFIP, but private flood insurance companies may offer higher limits or more flexible coverage options. Compare both types to see what fits your needs.

Flood risk is real, but you can protect your home and finances with the right coverage. Understanding flood insurance coverage requirements helps you make smart choices—before the waters rise.

Read More:

- Workers Compensation Insurance Costs: What You Need to Know

- Motorcycle Insurance for Young Riders: Essential Tips and Savings

- Pet Insurance Plans With Low Deductibles: Save More on Vet Bills

- Umbrella Insurance Policy Benefits: Protect Your Assets Today

- Best Renters Insurance Policies 2026: Top Picks for Maximum Protection

- Commercial Truck Insurance Coverage: Essential Guide for 2024

- Dental Insurance for Self-Employed: Maximize Your Coverage Today

- Medicare Supplement Insurance Plans: Your Guide to Smarter Coverage