Navigating health care in the United States can feel complicated, especially for older adults. Medicare helps cover many medical costs, but it doesn’t pay for everything. This is where Medicare Supplement Insurance Plans—often called Medigap—come in. Understanding these plans is important for anyone looking to protect their finances and get better health coverage. If you’re nearing retirement or already on Medicare, learning how Medigap works can help you make smart decisions for your health and wallet.

What Are Medicare Supplement Insurance Plans?

Medicare Supplement Insurance Plans are private insurance policies designed to fill the “gaps” in Original Medicare (Parts A and B). These gaps include deductibles, copayments, coinsurance, and sometimes emergency medical coverage outside the U.S. Medigap policies are standardized by the federal government, so each plan offers the same basic benefits no matter which insurance company sells it.

You must already have Original Medicare to buy a Medigap plan. Medigap does not work with Medicare Advantage (Part C). If you switch from Medicare Advantage to Original Medicare, you can apply for a Medigap plan, but acceptance may depend on your health and timing.

Why Consider A Medigap Plan?

Original Medicare covers about 80% of approved medical expenses, leaving you responsible for the remaining 20%. These costs can add up quickly, especially if you have frequent doctor visits or a hospital stay. Medigap plans help pay these leftover expenses, reducing your out-of-pocket costs.

- Financial protection: Avoid high bills from hospital stays or specialist visits.

- Freedom of choice: See any doctor or hospital that accepts Medicare nationwide.

- Predictable costs: Fixed monthly premiums make budgeting easier.

Many retirees find Medigap helpful for peace of mind and financial stability. According to the Kaiser Family Foundation, about 14 million people were enrolled in Medigap plans in 2023, showing their popularity among older adults.

How Medigap Works With Medicare

Medigap works as secondary insurance. Medicare pays its share first, and your Medigap plan pays some or all of the remaining costs. Here’s a simple example:

- You visit a doctor. The bill is $200.

- Medicare approves and pays 80% ($160).

- You owe 20% ($40).

- If your Medigap plan covers this copayment, you pay nothing or only a small fee.

Medigap plans do not cover prescription drugs, vision, dental, or hearing services. You must buy separate coverage for those needs.

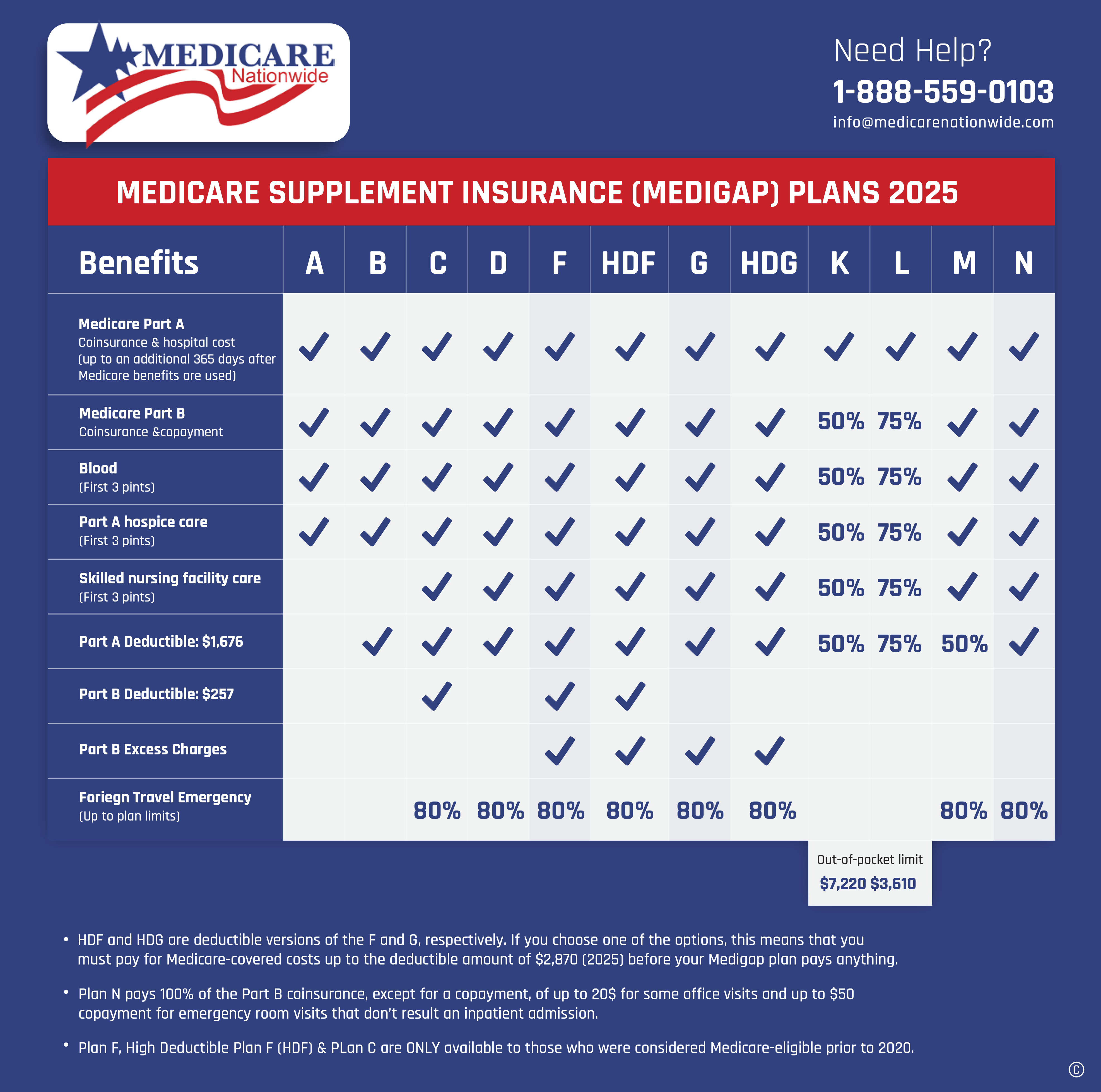

Types Of Medigap Plans

Medigap plans are labeled with letters (A, B, C, D, F, G, K, L, M, N). Each offers a different set of benefits. Not all plans are available in every state, and some are only for people who enrolled in Medicare before 2020.

Here’s a comparison of the most popular Medigap plans:

| Plan | Coverage Level | Monthly Premium (avg.) | Extra Features |

|---|---|---|---|

| Plan F | Comprehensive | $160-$230 | Foreign travel emergency |

| Plan G | High | $120-$200 | Similar to F, but excludes Part B deductible |

| Plan N | Moderate | $90-$150 | Lower premiums, some copays |

Plan F was the most popular, but it’s only available to those who qualified for Medicare before January 1, 2020. Plan G is now the top choice for new enrollees, offering nearly identical coverage except for the Part B deductible.

Credit: marylandmedicareoptions.com

What Does Each Plan Cover?

Each Medigap plan covers different “gaps.” Here’s a quick breakdown of what’s included:

| Benefit | Plan F | Plan G | Plan N |

|---|---|---|---|

| Part A coinsurance & hospital costs | Yes | Yes | Yes |

| Part B coinsurance/copay | Yes | Yes | Yes (with copays) |

| Blood (first 3 pints) | Yes | Yes | Yes |

| Part A hospice coinsurance | Yes | Yes | Yes |

| Part B deductible | Yes | No | No |

| Foreign travel emergency | Yes | Yes | Yes |

Plan N has lower premiums but requires copays for some office and emergency room visits. Plan G and Plan F cover almost all gaps except for the Part B deductible (only Plan F covers this).

Choosing The Right Medigap Plan

Picking a Medigap plan depends on your health, budget, and travel habits. Here are key factors to consider:

- Coverage needs: Do you visit doctors often? Want full protection for hospital bills? Choose a plan that matches your needs.

- Budget: Premiums vary, so compare costs carefully. Higher coverage usually means higher premiums.

- Travel: If you travel outside the U.S., pick a plan with foreign travel emergency coverage.

- Medical history: Some plans are only available if you qualified for Medicare before 2020.

- State rules: Medigap plans are standardized, but some states like Massachusetts, Minnesota, and Wisconsin have different rules.

Here’s a simple comparison to help you decide:

| Type of Person | Recommended Plan | Reason |

|---|---|---|

| Frequent traveler | Plan G or F | Foreign travel emergency |

| Budget-conscious | Plan N | Lower premium, copays manageable |

| Maximum coverage | Plan G | Almost all gaps covered |

How To Enroll In A Medigap Plan

You can apply for a Medigap plan through private insurance companies. The best time is during your Medigap Open Enrollment Period, which lasts six months from the first day you turn 65 and enroll in Medicare Part B. During this period:

- You cannot be turned down for health reasons.

- You get the best prices.

- Coverage starts immediately.

After this period, companies can ask about your health and may charge higher prices or deny coverage. Some states have extra protections, but timing is important.

Costs And Premiums

Medigap plans have monthly premiums in addition to your Medicare Part B premium. Premiums depend on:

- Plan letter: More coverage, higher cost.

- Location: Prices vary by state and city.

- Age: Some companies use age-based pricing.

- Health: If you apply outside open enrollment, health may affect cost.

The average Medigap premium ranges from $90 to $230 per month. Some people pay less, others pay more. Always shop around and compare at least three providers before choosing.

What’s Not Covered By Medigap

Medigap is great for covering medical gaps, but there are limits. Medigap does not cover:

- Prescription drugs: You need a separate Medicare Part D plan.

- Long-term care: Nursing home or assisted living costs are not included.

- Vision and dental: Routine exams, glasses, and dental care require other insurance.

- Hearing aids: Not covered by Medigap.

These limits are important. Many people mistakenly believe Medigap covers everything. Always review what’s included before buying.

Common Mistakes When Choosing Medigap

Many beginners make mistakes when picking a Medigap plan. Here are two non-obvious insights to avoid trouble:

- Assuming all plans are available everywhere. Some states limit choices, and not every insurance company sells every plan. Check your state options.

- Missing the open enrollment window. Applying after this period can mean higher costs or even denial based on pre-existing health conditions.

Another mistake: Not comparing prices between companies. Medigap plans are standardized, but premiums vary widely. Always compare before deciding.

Credit: medicarenationwide.com

Medigap Vs. Medicare Advantage

Some people confuse Medigap with Medicare Advantage (Part C). These are different:

- Medigap: Works with Original Medicare. Covers gaps, lets you choose any doctor nationwide.

- Medicare Advantage: Replaces Original Medicare. Offers extra benefits (like vision and dental), but limits you to network providers.

If you prefer flexibility and nationwide coverage, Medigap is usually a better choice. If you want extra benefits and are okay with network limits, Medicare Advantage may be right for you.

For more in-depth information, visit the official Medicare.gov website.

Tips For Getting The Most From Medigap

- Shop around: Compare plans and prices from different companies.

- Ask about discounts: Some companies offer discounts for spouses or nonsmokers.

- Check provider networks: While Medigap lets you see any provider, confirm your doctor accepts Medicare.

- Review annually: Your needs may change, so review your coverage each year.

Credit: www2.unitedamerican.com

Frequently Asked Questions

What Is The Difference Between Medigap And Medicare Advantage?

Medigap works with Original Medicare to cover gaps like copayments and deductibles. Medicare Advantage replaces Original Medicare and usually includes extra benefits such as vision, dental, and prescription drug coverage, but limits you to network providers.

When Can I Enroll In A Medigap Plan?

The best time to enroll is during your Medigap Open Enrollment Period—the six months after you turn 65 and sign up for Medicare Part B. During this time, you can’t be denied coverage or charged more due to health conditions.

Does Medigap Cover Prescription Drugs?

No. Medigap does not cover prescription drugs. You need to buy a separate Medicare Part D plan for drug coverage.

Can I Switch Medigap Plans Later?

Yes, you can switch plans, but after your open enrollment period, companies may ask about your health and could deny coverage or charge higher premiums. Some states offer more flexibility, so check local rules.

Are Medigap Premiums Tax-deductible?

In most cases, yes. Medigap premiums may be tax-deductible if your medical expenses are high enough. Always consult a tax professional for details.

Choosing the right Medicare Supplement Insurance Plan can make health care simpler and less stressful. Take time to compare your options, understand your needs, and shop smart. With careful planning, you can protect your health and your finances for years to come.

Read More:

- Workers Compensation Insurance Costs: What You Need to Know

- Motorcycle Insurance for Young Riders: Essential Tips and Savings

- Pet Insurance Plans With Low Deductibles: Save More on Vet Bills

- Flood Insurance Coverage Requirements: What Homeowners Must Know

- Umbrella Insurance Policy Benefits: Protect Your Assets Today

- Best Renters Insurance Policies 2026: Top Picks for Maximum Protection

- Commercial Truck Insurance Coverage: Essential Guide for 2024

- Dental Insurance for Self-Employed: Maximize Your Coverage Today